In present days we live in a world, where all items or assets or commodities can be used / purchased on easily available installments, called EMI. So, let us understand what is EMI and how does it work or affects us.

EMI is a financial term. It is the abbreviation for Equated Monthly Installment, which a borrower or purchaser is liable/required to pay at the equal intervals of time (generally each month) in return of using or purchasing an asset, home or even a commodity.

Definition

EMI or equated monthly installment, as the name suggests, is one part of the equally divided monthly outgoes to clear off an outstanding loan within a stipulated time frame.

Description

The EMI is dependent on multiple factors, such as:

- Principal borrowed

- Rate of interest

- Tenure of the loan

- Monthly/annual resting period

Various factors such as principal loan amount, tenure and the interest rate decides the amount of EMI. There has been an increased penetration of banks and financial institutions due to which there is huge availability of assets including home, car and many other appliances by way EMI. There are standard formulas by which EMI is calculated.

For a fixed interest rate loan, the EMI remains fixed for the entire tenure of the loan, provided there is no default or part-payment in between. The EMI is used to pay off both the principal and interest components of an outstanding loan. The first EMI has the highest interest component and the lowest principal component. With every subsequent EMI, the interest component keeps on reducing while the principal component keeps rising. Thus, the last EMI has the highest principal component and the lower interest component.

In case the borrower makes a pre-payment through the tenure of a running loan, either the subsequent EMIs get reduced or the original tenure of the loan gets reduced or a mix of both. The reverse happens when the borrower skips an EMI through the tenure of the loan (EMI holiday or cheque dishonor/bounce or insufficient balance in case of auto deduction of EMI or a default); in that case either the subsequent EMIs rise or the tenure of the loan increases or a mix of both, apart from inviting a financial penalty, if any.

Similarly, in case the rate of interest reduces through the tenure of the loan (as in the case of floating rate loans) the subsequent EMIs get reduced or the tenure of the loan falls or a mix of both. The reverse happens when the rate of interest rises.

EMI in Simple Term

In simple terms, if you buy an equipment worth Rs. 1.00 lac and you agree to pay back in 50 installments, then you will have to pay Rs. 2000/- per month towards the basic i.e. principal amount. Over and above that, you will have to keep on paying interest on the outstanding dues, till the full principal is repaid. EMI is a system wherein, the repayment of interest and principal amount has been equated over the repayment period. If this is not done and only principals are paid in equal installments and the interest is payable as due then in the initial years / months, the installments would be very high. So what happens in EMI is that the first / initial payment serves majorly interest and very less of principal while at the end of repayment period, principal is major and less of interest. So in the stated example you end up paying Rs. 2125.00 per month for 50 months.

As every coin has two sides, there are also two sides of buying through installments. So, let’s understand in detail.

Advantages of EMI

EMI is a blessing to the people, who sustain on a steady and limited source of income and are unable to pay off huge amount at a time. Listed here are some of the advantages of EMI:

01. Freedom and Power to Buy Expensive Utilities / Home:

- EMI provides chance to the consumers to buy expensive utilities / home which they otherwise, won’t be able to buy at one go as they may not have that huge amount at a particular time or one time.

- EMI helps us to buy anything and everything, whether it is expensive household items, gifts or jewellery for wedding, vehicles and even a house.

- Consumers purchase and enjoy the benefits, from day one as they get a chance to divide and pay the amount in form of monthly instalments and pay off easily later while using and enjoying it.

- This proves to be an advantage to traders and sellers too as they can easily sell such items to the buyers, which otherwise is difficult due to high onetime capital costs.

- The major benefit of buying anything through EMI is that you start enjoying the product or appliances from day one without making full payment. This is very important because if the same was not available through EMI, you could not have afforded the one-time price and therefore you would be kept away from enjoying it till the time till you save money for the same.

02. Wallet-Friendly:

- EMI helps in saving you from making a hole in your pocket as you only have to make minimal or fixed payment every month instead of paying huge sum of money at one go.

03. Flexibility:

- Depending upon the financial situation and income, EMI allows flexibility in the amount you want to pay for installment and the time duration during which you want to repay.

04. Absence of Any Middlemen:

- The EMI is paid is directly to the lender and there are no hassles of any middlemen.

05. Pay in Installments:

- EMI confers users with the liberty to pay a small fixed amount every month. This makes it easy for them to afford daily life commodities without burning a hole in their pockets. Moreover, many banks charge a very minimal charge as interest for most EMI schemes especially for commodities like air conditioner, mobiles and other gadgets.

Disadvantages of EMI

Listed below are some of the advantages of EMI:

01. Long-Term Debts:

- EMI is a long-term debt as one has to pay the instalments till, they finish paying off the principal amount as decided by the lender along with interest.

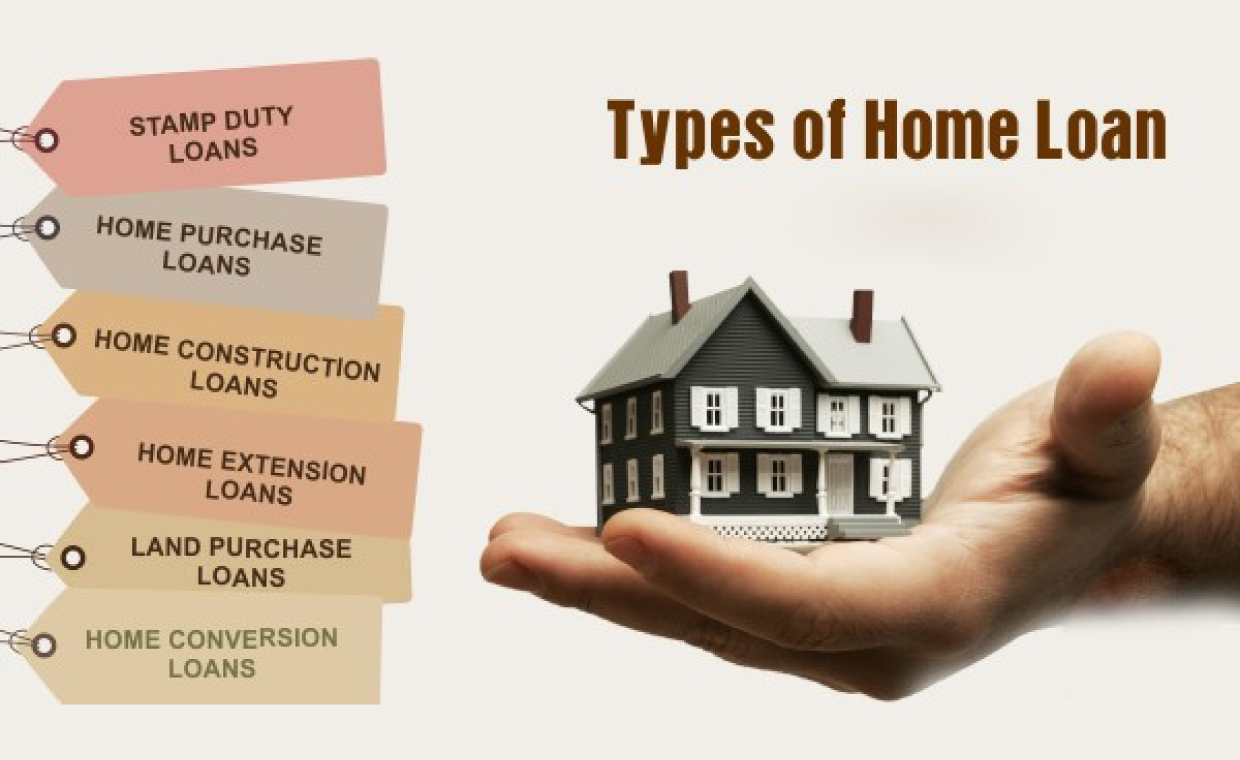

- Some loans such as home loans can take up to 20 / 30 years, which will restrict the users’ freedom to buy other luxurious items in future.

- Moreover, the person paying EMI lands up paying more amount than the principal amount, as the interest is generally applied on such schemes e.g. on a loan of Rs. 1.00 lac payable in 50 installments @ 10% rate of interest you would end up paying R.s 2125.00 per month i.e. Total Rs. 1,27,482.00 means Rs. 27,482.00 moreover for 50 months towards interest.

02. No Early Payment Option:

- Generally, the EMI schemes do not offer early payment options even if, the payee is willing to pay the principal amount before the decided tenure of payment.

- This will be a setback for the payee as he/she will end up paying more than principal amount because of interest charged.

03. Serious Consequences:

- Different EMI schemes observe strict rules and regulation, if you do not pay or are irregular in paying.

- There are various serious consequences such as repossession of the purchased item, foreclosure, penalties or strict legal actions which may occur due to non-payment of EMI.

- It is therefore, suggested to the consumers / home owners to read the terms and conditions before opting for such EMI schemes, to avoid losing the mortgaged item or facing any legal actions leading to problems.

- Before you finalize the deal, always check the repossession cause i.e. under what and which circumstances the lender can repossess the same as in such event if agreement is one sided it will put you in a situation where you will lose both EMIs paid and the product / home as well.

- Please also be careful while giving the post-dated cheques towards EMIs as guarantee. Remember, failure to honour the cheque may land you in jail. Hence never over trade and go beyond your limit and capacity.

- Some finance companies employ “Mafias” to recover the money. They not only insult you but will torture you, beyond a limit. So always check the history of lender before closing deal and avoid such companies. Always prefer reputed, honoured and dignified financial institutions.

04. Bad as a Habit:

- Nowadays, most of the products are financed by sellers or manufactures with the help of financial institutions. Home, the temptation to buy everything on day one is big. Hence buying everything on EMI is a bad habit and the day may come that your EMI for all things, taken together would exceed your repayment capacity and income.

- Very important caution and one very important thing that one must never forget is to keep in mind that if you buy a product or even a home, on 5 years or 10 years instalments, than the you must remember that you are enjoying property out of the income which you are going to earn after 5 / 10 years and not the current income. While this may not look like a problem but when you think of losing your job or business or have a fear of loss of income, then this will keep you in constant stress rather than enjoying the product or property and will increase your Blood Pressure.

05. Costly Overall:

- One should be vigilant that, most of the financial institutions financing small products charge reasonably higher rate of interest than prevailing otherwise in the market.

- Please assure and ascertain that there are no hidden charges other than the principal and interest. Please also check penal charges in case of delay or defaults in paying EMI.

06. Additional Costs:

Additional costs in terms of interest. One doesn’t have to pay interest if the payment is made all at once.

07. Prepayment Penalty:

Several institutions do not allow prepayment and even if they do there will be serious penalties that one will have to pay for prepayment.

Factors Affecting the EMI

There are various factors which affects the EMI with the change in period of time. Some of them are mentioned as follows:

01. Change in Interest During Repayment Duration:

- There is possibility that there would be change in the interest rate multiple times during tenure of a loan due to macro-economic changes in nation.

- Rate of interest may vary between range of rates, in case of floating interest loans.

- So, if your home loan is under floating interest rate then it is likely that your EMI will get revised over a period of time (Higher or Lower).

- To calculate the floating EMIs, you can take help of various EMI calculator available online.

02. Extra Payment/Prepayment of Principal Amount:

- Partial loan payment in buckets will affect the EMI as it will decrease the amount overdue on the loan.

- Most of the banks allow to prepay the loan prematurely.

- It may attract penalty of 1% to 3% of the remaining principal amount for pre-payment.

03. Change in Loan Duration:

- There can be negotiations with the current lender for better or extended loan tenure or you may move to a next lender who will provide you better repayment tenure.

- Longer the tenure (duration), less will be the EMI every month which will leave more cash in your hand to spend but paying loan for a longer tenure will increase interest and hence you will end up paying more.

04. Flexible Option of Repayment:

- Two types of repayment options are available with each loan.

- STEP-UP OPTION: In this option, the EMI is initially lower and will increase over a period of time.

- It is quite beneficial for those, who are at the beginning of the careers. Hence as their income increases with increase in the time period, they can opt to pay higher.

- STEP-DOWN OPTION: In this option, the EMI is initially higher and will decrease with time.

No Cost EMI

The price you pay for a ‘no cost EMI’ In 2013, the Reserve Bank of India (RBI) banned banks from offering 0% EMI scheme on retail products. So, banks try to come up with a variant of the option. No cost EMI sounds like you don’t have to pay any interest on the loan, but in reality, you do.

Summing up, EMI is light on pocket and leads to smooth payment but will eventually lead to higher payment with increase in time due to interest charged on it.

It is always advisable to read the terms and conditions of the agreement before signing for EMI schemes, in order to be on safer side and free from hidden charges or tough conditions.

EMI allows to pay on monthly basis. Instead of paying the total sum at one go, you can break the same into smaller amount and pay it monthly.

It is a good option to purchase any product because:

- It increases your affordability

- You can raise your budget

- It does not hamper your monthly budget

There are various products that are usually purchased in EMI, due to their high costs. Consumer durables, digital products, lifestyle products, clothes & accessories and more can be purchased on easy EMIs.

Hope this article would have provided you the basic knowledge of EMI.